IFRS 15 Revenue from Contracts with Customers

The IASB- International Accounting Standards Board Issued IFRS 15 “Revenue from contracts” to guide accounting for revenue from contracts with customers. The new standard became effective in January 2018 financial year onwards.

The core principle of IFRS 15 is that “the revenue recognition must represent the transfer of goods (promised) or services to customers in an amount that reflects the consideration to which the company expects/ received to be entitled in exchange for those goods or services”.

The transfer of goods or services is based on the transfer of control to the customer. The transfer may occur at a point in time (when a goods/service is delivered) or over time (a service is rendered or as goods are being constructed).

The IFRS 15 “Revenue from contract with customers” eliminates different treatments in how businesses and industries handle accounting for similar transactions. This difference in the accounting and disclosures in financial reporting has made it difficult for investors and other financial statement stakeholders to compare results (benchmarking) across industries and even companies within the same Industry.

IFRS 15 “Contract with customers” Replaces the following standards and interpretations

- IAS 18- “Revenue”

- IAS 11 -“Construction contracts

- SIC 31 -“Barter transaction involving advertising services.”

- IFRIC 13- “Customer loyalty programs.”

- IFRIC 15 -“Agreement for the construction of the real estate.”

- IFRIC 18 -“Transaction of assets from customers

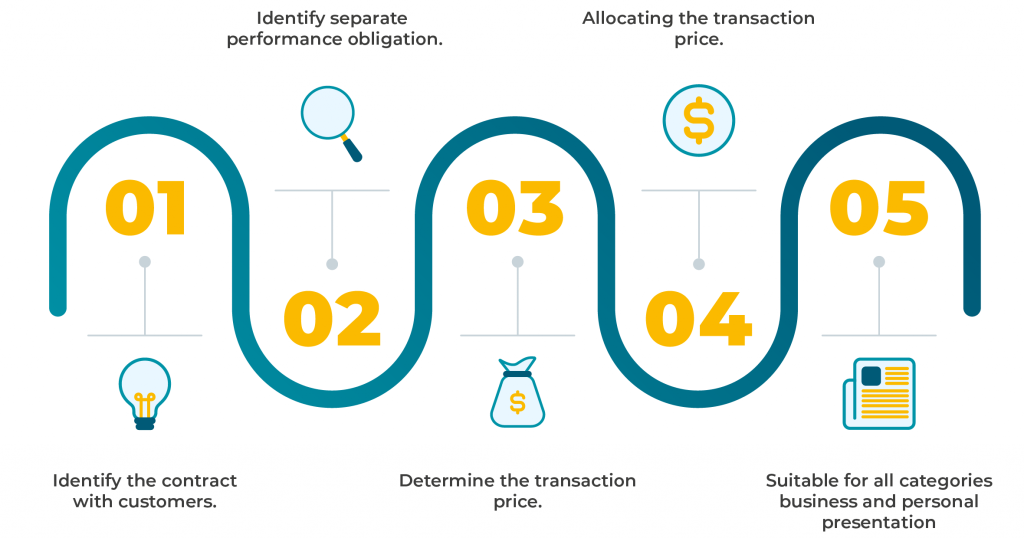

IFRS 16 Overview: 5 Step Model

Registered and Approved Auditor in UAE

Audit Service in Mainland

Audit Service in Free zone

net synergies realized above the initial target in the first year.

“Partnering with Execor was a game-changer for us. They took the time to understand our challenges and helped us streamline our operations for success.”

reduction in time spent on reporting was realized

“Execor has been instrumental in our growth. Their team took the time to truly understand our needs and helped us eliminate inefficiencies.”

reduction in errors and streamlining data management through automation.

Our Latest Insights

About the Author

A CMA holder and certifications from the London School of Economics (LSE), Sumesh Krishna brings over 25 years of auditing and business consultancy expertise. As the head of HLB HAMT’s Audit & Assurance division and HLB International’s Global Not-For-Profit Leader, he specializes in modernizing audit processes, integrating digital tools like RPA and ISQM standards, and ensuring compliance with IFRS and internal control frameworks. His leadership is instrumental in delivering high-quality, technology-driven assurance services.